Disclaimer: This is not financial advice. I’m sharing my own research and analysis for educational purposes. I hold a position in DVLT. Always do your own due diligence before making any investment decisions.

What Is Datavault AI?

Datavault AI (NASDAQ: DVLT) is a data sciences and technology company headquartered in Philadelphia, PA. The company operates through two divisions: a Data Science Division focused on Web 3.0 data monetization, tokenization, and high-performance computing (HPC), and an Acoustic Science Division built around its WiSA, ADIO, and Sumerian patented wireless audio technologies.

If that sounds like a lot of buzzwords packed into one company, and you’re not wrong. And that’s part of what makes DVLT both interesting and risky.

The company was formerly known as WiSA Technologies, a wireless audio company that rebranded to Datavault AI in February 2025 to reflect its pivot toward AI-driven data management and monetization. They also acquired CompuSystems’ live events technology assets in May 2025, adding registration, data analytics, and lead management services to the mix.

The Numbers: Where the Money Comes From

Let’s start with what matters most: the financials.

Revenue Growth

DVLT’s revenue story is, on the surface, one of the most dramatic growth trajectories in the micro-cap space:

- FY 2024 revenue: $2.7 million

- Q2 2025 recognized revenue: $1.7 million (a roughly 467% year-over-year increase)

- Q3 2025 revenue: $2.9 million (up from $1.2 million in Q3 2024)

- 9-month 2025 revenue (through Sept 30): $5.3 million

- Preliminary FY 2025 revenue estimate (unaudited): $38–$40 million

- FY 2026 guidance: $40–$50 million (earlier CEO letter targeted $200 million)

That preliminary 2025 figure implies massive Q4 acceleration. Going from $5.3 million through nine months to $38–$40 million for the full year means roughly $33–$35 million in Q4 alone. Management attributes this to tech-licensing fees and tokenization deals, including $49 million in tokenization and licensing deals announced in Q4.

This is where investors need to pay very close attention. That kind of hockey-stick revenue concentration in a single quarter, driven largely by tokenization deals, demands scrutiny. Are these recurring revenue streams or one-time licensing events? The audited financials will tell the real story.

Profitability (or Lack Thereof)

Revenue growth is exciting, but the bottom line tells a different story:

- Q3 2025 gross profit: $0.1 million on $2.9 million revenue (roughly 3.4% gross margin)

- Q3 2025 operating loss: $(14.8) million

- Q3 2025 net loss: $(33.0) million

- 9-month 2025 net loss: $(79.7) million

- Current P/E ratio: Negative (-0.52)

The company is burning cash significantly. Operating expenses of $14.9 million in Q3 alone dwarf the revenue, and the net loss is amplified by fair value changes on convertible notes and debt activity.

Balance Sheet

As of September 30, 2025:

- Cash and equivalents: $1.7 million

- Crypto assets: $8.1 million

- Total assets: $138.7 million

- Intangible assets: $97.5 million (largely from the CompuSystems acquisition)

- Goodwill: $19.1 million

- Total liabilities: $39.2 million

- Stockholders’ equity: $99.5 million

The balance sheet is asset-heavy, but the majority of those assets are intangibles and goodwill. Not cash. With only $1.7 million in liquid cash, the company needs external capital to fund operations. They secured a $150 million strategic investment commitment to support supercomputing and tokenization initiatives, but the terms and drawdown schedule matter.

The Business: What Are They Actually Building?

Data Science Division

This is the growth engine. Datavault’s data science arm focuses on:

- Real-world asset (RWA) tokenization: converting physical assets into blockchain-based digital tokens for trading and monetization

- Information Data Exchange (IDE): enabling digital twins and secure licensing of name, image, and likeness (NIL)

- High-performance computing (HPC): providing supercomputing infrastructure for data processing

- Edge network deployment (the company claims to be on track for fully operational nodes across 100+ cities in the second half of 2026)

The tokenization angle is the most aggressive growth bet. Management has highlighted $49 million in tokenization and licensing deals in Q4 2025, and the 100-city edge network rollout could be transformative if executed (emphasis on “if”).

Acoustic Science Division

The legacy WiSA business remains, providing patented wireless audio technologies. While this division generates revenue through components and consumer audio products, it’s not the growth driver. Think of it as the foundation that keeps the lights on while the data science division scales.

Live Events (CompuSystems Acquisition)

The May 2025 acquisition of CompuSystems brought $2.2 million in Q3 2025 revenue, making it the largest revenue contributor for that quarter. This business provides registration, data analytics, and lead management for trade shows and corporate events. It’s a real business with real customers, and it provides a more predictable revenue base compared to tokenization deals.

Key Catalysts to Watch

1. Audited FY 2025 Financials The preliminary $38–$40 million revenue figure is unaudited. The audited 10-K filing (expected in spring 2026) will either validate the growth story or raise red flags. This is the single most important near-term catalyst.

2. 100-City Edge Network Deployment Management targets operational nodes across 100+ U.S. cities in H2 2026. If executed, this infrastructure could drive recurring revenue from data processing and HPC services. If delayed, it undermines the growth narrative.

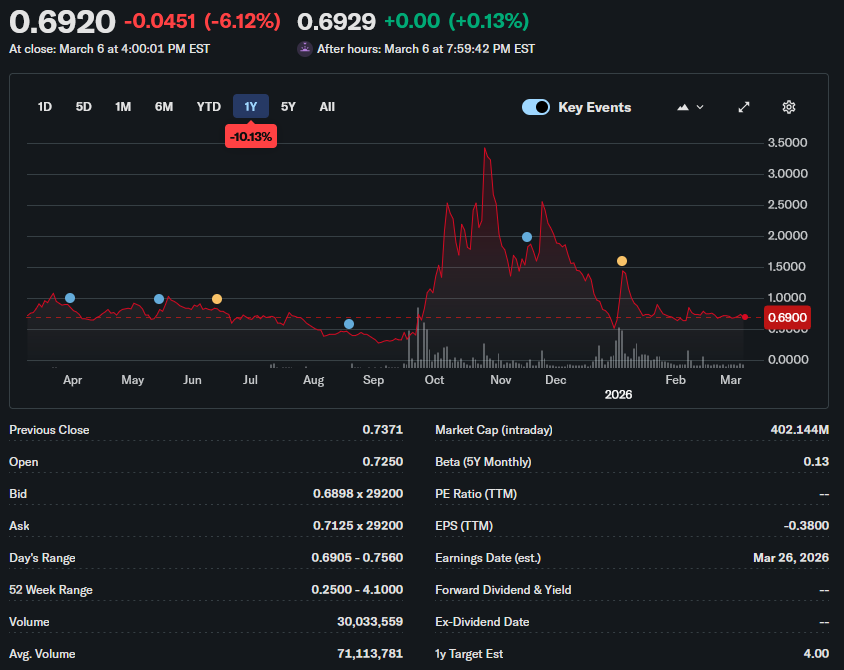

3. Nasdaq Compliance DVLT received a bid price deficiency notice in May 2025 for trading below $1.00. The stock currently trades around $0.70. Failure to regain compliance could result in delisting, which would be devastating for liquidity and institutional interest.

4. 2026 Revenue Guidance The company has given conflicting 2026 guidance. The CEO letter mentioned $200 million, while the November investor update targeted $40–$50 million. Clarity on realistic expectations matters.

5. Tokenization Deal Conversion Whether Q4 2025’s tokenization deals translate into recognized revenue on the audited financials, and whether similar deals continue, will determine if this is a sustainable business model or a one-time event.

The Risks: What Could Go Wrong

Dilution

The company authorized increasing total shares from 320 million to 2.02 billion in November 2025. That’s a massive expansion of authorized capital. Combined with the Scilex investment involving common stock and pre-funded warrants, existing shareholders face significant dilution risk. There’s also an active S-3 registration for 5 million shares for resale.

Going Concern Risk

With only $1.7 million in cash as of Q3 2025 and quarterly operating losses exceeding $14 million, the company’s ability to continue as a going concern depends on external financing. If capital markets tighten or investor sentiment shifts, funding could dry up.

Revenue Quality

The dramatic Q4 2025 revenue spike from tokenization deals raises questions about sustainability. Tokenization and licensing revenue can be lumpy and non-recurring. Investors should scrutinize the audited financials for revenue recognition policies and the nature of these transactions.

Execution Risk

The business plan is ambitious: 100-city edge network, global expansion across multiple continents, partnerships in sports, biotech, education, fintech, real estate, healthcare, and energy. Executing across this many verticals simultaneously with limited cash is extremely challenging.

Meme Coin Integration

The company has integrated a “Dream Bowl Meme Coin” into its ecosystem, including making warrant exercise conditional on holding meme coin tokens. This is unconventional at best and a red flag at worst. Combining traditional equity instruments with meme coin requirements introduces unnecessary complexity and reputational risk.

Stock Price Behavior

Market reaction to recent AI-related announcements has been consistently negative, with an average one-day move of -3.42% across the last five AI-tagged press releases. The market is skeptical, and press releases aren’t translating into price appreciation.

Bull Case

If you believe in DVLT, here’s the case:

- Revenue is genuinely inflecting. Going from $2.7 million to potentially $38–$40 million in one year is transformative if the numbers hold up under audit.

- The tokenization market is early. RWA tokenization is projected to be a multi-trillion dollar opportunity. If Datavault captures even a fraction, the current market cap (roughly $400 million) could be a rounding error.

- The edge network is a moat. 100+ city deployment of HPC nodes creates physical infrastructure that competitors can’t replicate overnight.

- The CompuSystems acquisition provides real revenue. Unlike the tokenization business, live events is a proven business with existing customers.

- The stock is cheap. At $0.70 per share with a 52-week range of $0.25–$4.10, there’s significant upside if the business executes.

Bear Case

If you’re skeptical, here’s the case:

- The numbers don’t add up yet. How does a company go from $5.3 million through nine months to $38–$40 million for the full year? Until audited financials confirm this, it’s just a management estimate.

- Cash burn is unsustainable. $(79.7) million in net losses through nine months with $1.7 million in cash means constant dilution to survive.

- The pivot from WiSA to Datavault AI is a rebrand, not a transformation. The core business is still small, and the AI/Web3/tokenization narrative may be more marketing than substance.

- Meme coin integration is a serious red flag. Legitimate technology companies don’t typically tie equity instruments to meme coin ownership.

- Nasdaq delisting risk is real. Trading at $0.70 with the compliance clock ticking creates a potentially permanent liquidity problem.

- Insiders are selling. The CFO sold shares in November 2025 (for tax purposes, but still, not buying).

My Take

DVLT is one of those stocks where the gap between the bull case and the bear case is enormous. If the audited FY 2025 financials confirm the $38–$40 million preliminary revenue figure and the company demonstrates a clear path to recurring revenue from tokenization and edge computing, this could be significantly undervalued.

But the risks are just as real. The cash position is dangerously low, the authorized share count expansion signals more dilution ahead, and the meme coin integration raises governance questions that shouldn’t exist in a publicly traded company.

What I’m watching for:

- The audited 10-K filing. This is make or break

- Q1 2026 revenue trajectory. Does the momentum continue, or was Q4 a one-time event?

- Nasdaq compliance resolution

- Concrete progress on the 100-city edge network (not just press releases, not just press releases, but actual deployment milestones)

This is a high-risk, high-reward micro-cap. Position sizing should reflect that.

What do you think about DVLT? Am I missing something in this analysis? Drop a comment below or reach out on the newsletter. I read every reply.

If you found this useful, consider subscribing. I publish deep dives like this whenever I find a stock worth taking apart.